The global rigid plastic packaging market, valued at $220.2 billion in 2025, is set to expand to $262.7 billion by 2030, growing at a compound annual rate of 3.6%, according to the latest report from Smithers, The Future of Rigid Plastic Packaging to 2030.

The study highlights that improving recycling systems, managing volatile raw material costs and embracing new technologies will be among the top priorities for the sector in the coming five years. Smithers says demand will taper in mature regions, particularly Western Europe, but this will be offset by growth in developing economies where modern retail infrastructure and packaged goods consumption are on the rise.

David Platt, author of the report, said that rigid plastic packaging is broadly defined as “the manufacture, supply and conversion of plastics used separately or in combination for primary retail food packaging and non-food applications, such as beverages, pet food, medical items and pharmaceuticals, cosmetics and toiletries, household care and for industrial/other packaging.”

Platt noted that the industry has long benefitted from rigid plastics' role as a lightweight, cost-effective and high-performance alternative to traditional materials – but is now facing mounting pressure to address environmental impacts.

Sustainability front and centre

Platt said environmental concerns are “forcing companies to look for innovative ways to design more sustainable and eco-friendly product packaging, often at the expense of rigid plastics.” He pointed to a mix of strategies already underway, including redesign for recycling, weight reduction, use of bioplastics, and ensuring packaging contains recycled material.

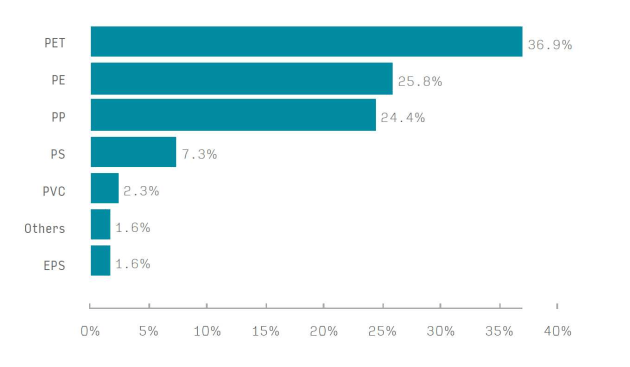

The Smithers forecast anticipates a wider use of mono-layer rigid packs to enhance recyclability, paired with new coatings that can replicate the barrier properties of multi-layer bottles. PET, already the most widely used polymer with 36.9% market share in 2025, is expected to grow further thanks to demand in beverage, ready-meal and pharmaceutical applications. Meanwhile, polypropylene (PP) is gaining ground as a cost-effective substitute for PE and PS in several segments, with new clarified PP grades opening opportunities in blow moulded bottles.

Thermoforming takes the lead

While blow moulding remains the largest production process, thermoforming is tipped as the fastest-growing technology.

“The growth of thermoforming is mainly due to demand for single-serve packs and the versatility and speed of machinery that enables rapid changeovers,” Platt explained.

This aligns with wider shifts in consumer behaviour. The rise of single-serve convenience formats, combined with the efficiency advantages of thermoforming, is positioning it as a critical growth driver across the forecast period.

Modern retail drives uptake

Another key factor in demand is the global rise of modern retailing. Platt noted that centralised grocery formats “have inevitably led to higher levels of packaging with extended shelf life, particularly for fresh foods, chilled foods and ready meals.”

Rigid plastics are also capturing share in developing markets, where retail chains are spreading and consumers are moving away from unpackaged goods. “Rigid plastic packaging has benefited from this trend towards packaged products that offer hygiene, convenience and longer shelf life,” Platt said.

Balancing headwinds

Despite the positive outlook, challenges remain. Volatile petroleum-based raw material costs continue to pressure margins, while flexible packaging formats such as stand-up pouches pose competition in some applications. However, Platt noted that flexible multi-material laminates are themselves under scrutiny for limited recyclability, which could strengthen rigid plastic’s position.

“The global introduction of regulations regarding plastic usage creates a challenge for the industry as companies need to comply with laws, invest in alternatives and reevaluate their packaging portfolios,” he added.

Market outlook

By 2030, rigid plastics will account for 80.8 million metric tons of material use worldwide, with PET, PE and PP together dominating more than 85% of demand. Beverage sector developments – including in-house bottle blowing by major brand owners and co-location of bottle-making operations with brand sites – will continue to deliver efficiencies and reshape supply chains.

For companies across the value chain, Smithers’ latest report makes it clear that while rigid plastics remain a mainstay of the packaging industry, the next five years will be defined by how effectively the sector integrates recyclability, manages cost volatility and adapts to the structural changes in retail and consumer behaviour.

The Future of Rigid Plastic Packaging to 2030 is available from Smithers for US$6,750 (€6,350, £5,475).