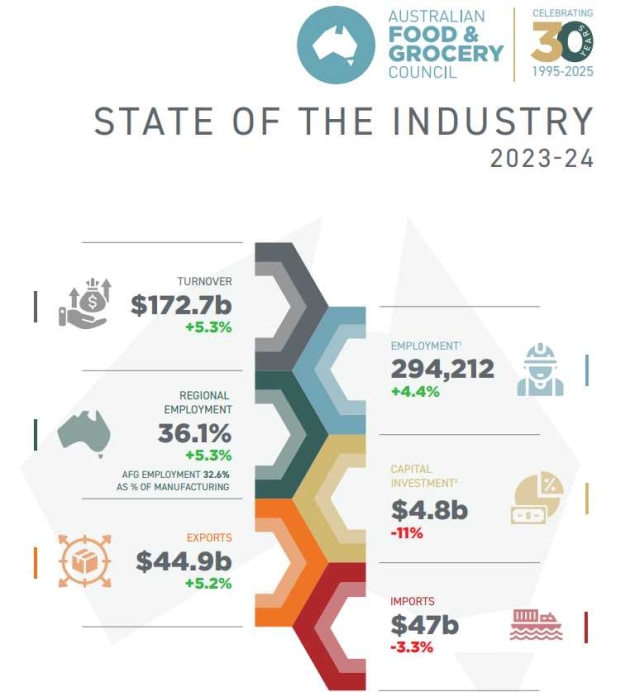

Australia’s food and grocery manufacturing sector – valued at $173 billion – has again delivered solid growth, with turnover, exports, and jobs all on the rise. However, industry leaders warn that productivity gains and renewed capital investment are urgently needed to unlock the sector’s full potential and ensure its competitiveness.

The Australian Food and Grocery Council’s (AFGC) State of the Industry 2023–24 report shows sector turnover up 5.3% to $173 billion, with employment growing 4.4% to almost 300,000 – over a third in regional areas. Exports increased 5.2%, and imports fell 3.3%, strengthening Australia’s trade balance. The United States overtook China as the top export market.

AFGC CEO Colm Maguire says the sector is well positioned to contribute to the government’s “Future Made in Australia” vision but must address investment decline – down 11% to $3.8 billion – and high operating costs. “With the right policy settings and strategic support, food and grocery manufacturing will continue to boost Australia’s economy – driving regional jobs, underpinning Australia as a proud manufacturing nation, and securing our food and grocery supply,” he said.

Productivity: A national priority

AFGC Chair Bernie Brookes says productivity gains are central to growth, and the government’s recent recognition of the sector in its national productivity agenda is timely. The Council is calling for reduced regulatory burdens, stronger supply chain and transport infrastructure, and reliable, affordable energy supply.

The sector has set an ambition to grow to $250 billion by 2030 – a target that depends on targeted investment, innovation, and smart collaboration between industry and government. Energy remains a key barrier, with rising costs threatening both competitiveness and long-term viability.

Supply chain pressures and opportunities for automation

The AFGC’s earlier 5 Big Trends Shaping Food and Grocery Supply Chains report underscores the urgency. Cost reduction now outranks customer satisfaction as the top supply chain priority, with energy, materials, labour, and transport costs biting into margins. Disruptions from extreme weather events and infrastructure failures continue to cause delays, reinforcing calls for greater investment in freight networks.

The survey also revealed that AI and automation are set to play a larger role in supply chain management, from demand forecasting to warehouse robotics. However, a shortage of skilled workers is slowing adoption. Sustainability remains a parallel priority, with new regulatory requirements driving investment in packaging reform, emissions reporting, and energy efficiency measures.

For APPMA members and the wider OEM market, these trends point to opportunities for machinery innovation that can help food and grocery manufacturers lift productivity, cut costs, and build resilience. Solutions that integrate automation, improve energy efficiency, and support sustainability will be in high demand as the sector navigates cost pressures and capacity constraints.