Australasia’s packaging and processing machinery sector entered 2025 with a cautiously optimistic outlook, buoyed by resilient demand across food, beverage and emerging categories, and supported by continued investment in automation and system upgrades.

The latest data from the 2025 Guide to Global Markets – produced by PMMI and co-sponsored by APPMA – reveals an industry shaped by global economic volatility, accelerating sustainability regulations and shifting consumption patterns, but still primed for growth across multiple equipment categories.

Global momentum sets the context

Packaging and processing machinery remains a strong global market, valued at €55.7 billion in 2024 and forecast to reach €66.6 billion by 2029, reflecting a CAGR of 3.6 per cent. Growth is broad-based, with Asia leading global demand at 37 per cent of market share, while the EU and North America hold roughly a quarter each. Emerging regions – particularly Latin America and Africa/Oceania – are outpacing mature markets in percentage growth, both tracking at or above 4 per cent CAGR through 2029.

Across machine types, Filling & Dosing and Form–Fill–Seal (FFS) equipment dominate global revenues, together accounting for nearly €23 billion in 2024. Strong growth is forecast in palletising, inspection, secondary packaging systems, and labelling, reflecting automation adoption and labour-efficiency priorities in both developed and emerging markets.

The report also underlines a global packaging market exceeding 4 trillion units, driven by flexible packaging, PET, and metal cans – all critical influencers of machinery demand. Sustainability regulations, recycled content targets and packaging redesign trends are reshaping equipment requirements across all regions.

Australasia in focus: A market that punches above its weight

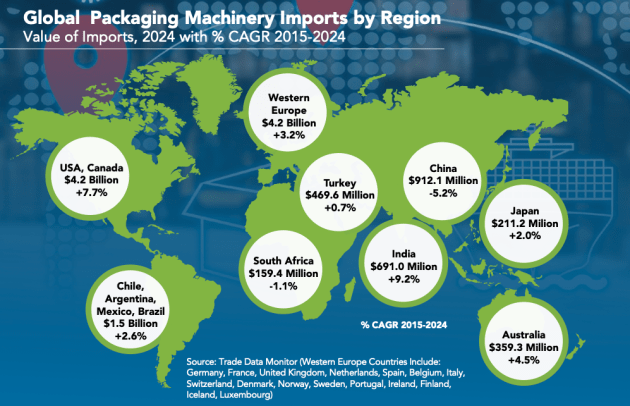

Australasia represents a relatively small share of global packaging consumption – 42.7 billion units in 2024 – yet it remains an important, high-value machinery market due to its advanced manufacturing base. The region imported US$359.3 million (AUD 551.8m) in packaging machinery in 2024, a notable 20.1 per cent increase on the previous year, signalling renewed investment momentum across food, beverage, household and pharmaceutical sectors.

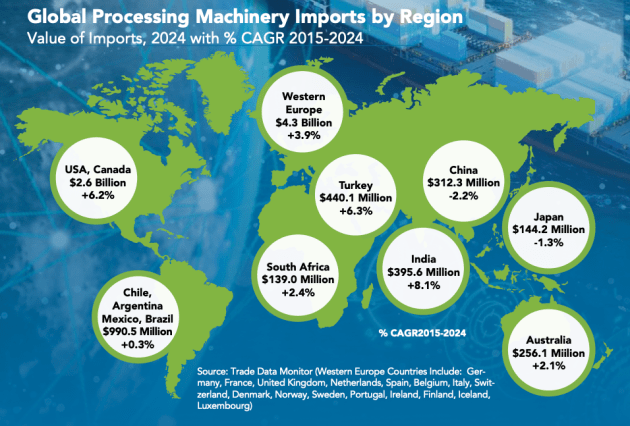

Processing machinery imports totalled US$256.1 million in 2024 (AUD 393.36m), reflecting a longer-term trend of upgrading production lines to meet stricter safety, hygiene, traceability and export-market requirements.

Across both packaging and processing equipment categories, Germany, Italy, the United States, the Netherlands and China remain Australia’s most significant machinery suppliers, mirroring global technology leadership and competitive positioning in automation, robotics, vision systems and advanced filling, sealing and palletising systems.

Sector performance: Food and beverage lead demand

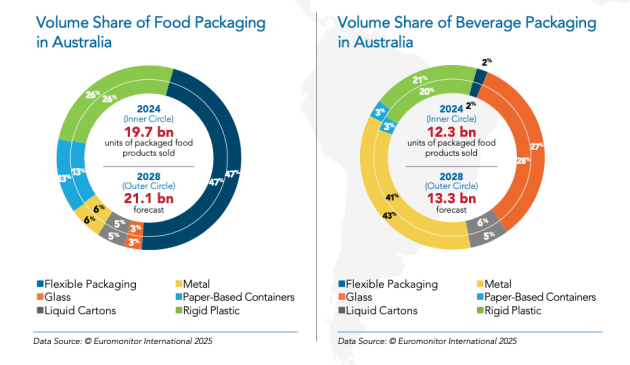

The Australasian market’s machinery demand closely aligns with trends in packaged food and beverage, which together represent the bulk of packaging volume. In Australia specifically, packaged food sales reached 19.7 billion units in 2024, forecast to grow to 21.1 billion by 2028, while beverages will increase from 12.3 billion to 13.3 billion units over the same period.

Top growth categories reflect evolving consumer behaviour:

- Premium fresh coffee, non-cola carbonates and bottled water show strong absolute volume increases

- Meat and seafood substitutes, tequila/mezcal, and instant tea show notable CAGR growth

- Flexible packaging, rigid plastic and metal cans remain the dominant substrate groups across both food and beverage applications

These consumption shifts directly influence equipment spending. Increased throughput requirements in bottled water and RTD beverages, for example, drive investment in high-speed filling, capping, shrink-wrapping, palletising and inspection systems. Growth in plant-based and specialty food categories increases demand for flexible FFS, multi-head weighing, tray sealing and MAP technologies.

Global trends shaping local investment

The report identifies several global mega-trends that are strongly influencing Australasian machinery priorities:

- Circularity and sustainability requirements

With recycled content targets, EPR schemes and redesigned packaging formats proliferating worldwide, machinery investment increasingly focuses on adaptability. Equipment must handle:

- rPET bottles

- Lightweighted plastics

- Recyclable mono-material films

- Recycled paper and fibre-based substrates

This drives demand for advanced controls, precision dosing, forming tolerances and more sensitive inspection capabilities.

- Continued rise of flexible packaging

Flexible plastics remain the world’s most used pack format, delivering 31 per cent of total volume in 2024. For Australasian manufacturers supplying export markets, flexibility in machinery – rapid changeovers, digital controls, and material-agnostic sealing systems – is crucial.

- Automation and labour efficiency

With labour shortages continuing across ANZ, the strongest machinery growth categories globally – palletising (up to 4.1 per cent CAGR) and handling/inspection – align perfectly with local operational needs. Robotics-integrated packaging lines are increasingly viewed as essential rather than optional.

- E-commerce packaging demands

Globally, protective, durable, convenient packaging formats continue to surge, influencing demand for case-packing, cushioning, sealing, coding and traceability systems. Australasian food and beverage exporters, as well as FMCG brands serving domestic e-commerce, mirror these needs.

Opportunities and challenges for the ANZ machinery sector

Opportunities

- Export growth: Asia–Pacific posting strong packaging demand (2.8 per cent CAGR) presents a major opportunity for Australian OEMs and integrators.

- Sustainability-driven upgrades: New materials and regulatory frameworks are accelerating line optimisation, not delaying it.

- High-value segments: Pharmaceuticals, nutraceuticals and specialty foods show strong machinery demand globally and locally.

- Automation integration: Growth in palletising and inspection technologies supports integrators and machine builders with strong robotics capabilities.

Challenges

- Competitive import environment: Europe and China continue to strengthen exports, setting high expectations for technology, pricing and support.

- Cost pressures: Rising input costs and tight capital expenditure budgets require suppliers to demonstrate clear ROI.

- Skills shortages: Integrators report ongoing difficulty recruiting automation engineers, line technicians and service specialists.

Outlook

Despite economic caution, the Australasian packaging and processing machinery market is positioned for sustained medium-term growth. Driven by a modernising manufacturing base, evolving consumer preferences and pressing sustainability imperatives, the region continues to invest in advanced equipment that boosts efficiency, quality and competitiveness.

In the context of global growth, Australasia remains small but strategically important – technologically advanced, export-oriented, and increasingly aligned with global circular-economy mandates. For OEMs, integrators and suppliers across the machinery landscape, the 2025–2029 period promises a landscape of continuing opportunity supported by strong fundamentals.